//hanabi-1

While the industry gravitates toward increasingly large models, our research has revealed that financial market prediction benefits from a more specialized, compact architecture. Hanabi-1 demonstrates how targeted design can outperform brute-force approaches in specific domains like financial time series analysis

With 16.4 million parameter model consists of:

- 8 transformer layers with multi-head attention mechanisms

- 384-dimensional hidden states throughout the network

- Multiple specialized predictive pathways for direction, volatility, price change, and spread

- Batch normalization rather than layer normalization for better training dynamics

- Focal loss implementation to address inherent class imbalance

The compact size enables faster inference times and allows us to deploy models at the edge for real-time decision making—critical for high-frequency market environments.

Mathematical Foundations: Functions and Formulas

Positional Encoding

To help the transformer understand sequence ordering, we implement sinusoidal positional encoding:

Where pos is the position within the sequence and i is the dimension index.

Focal Loss for Direction Prediction

To address the severe class imbalance in financial market direction prediction, we implemented Focal Loss:

Where p_t is the model's estimated probability for the correct class and γ is the focusing parameter (set to 2.0 in Hanabi-1). This loss function down-weights the contribution of easy examples, allowing the model to focus on harder cases.

Confidence Calibration

A key innovation in Hanabi-1 is our confidence-aware prediction system:

Where p is the predicted probability and threshold is our calibrated decision boundary (0.5). This allows users to filter predictions based on confidence levels, dramatically improving accuracy in high-confidence scenario.

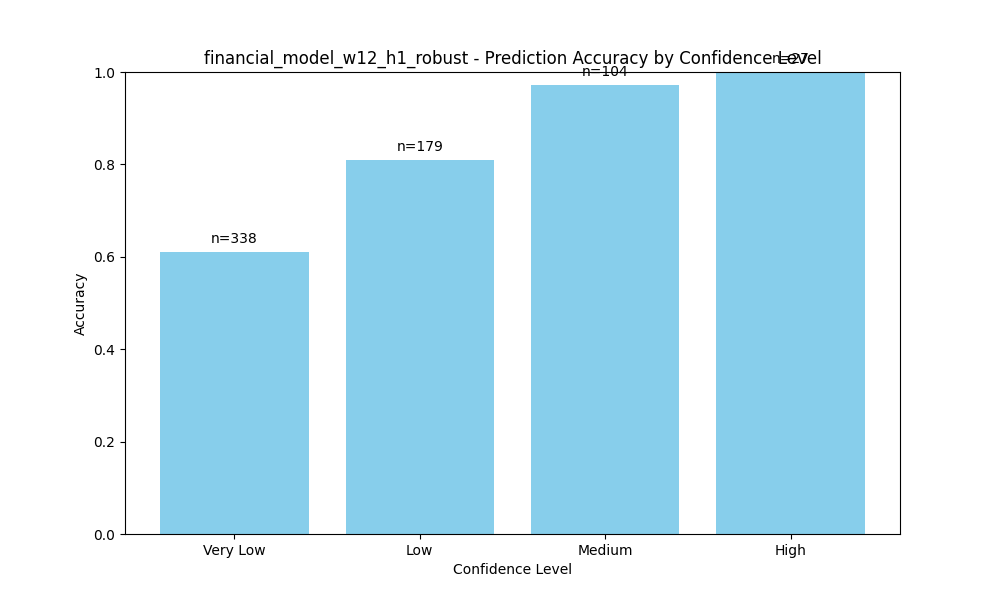

Confidence vs Accuracy

Confidence vs Accuracy

As shown above, predictions with "High" confidence achieve nearly 100% accuracy, while "Very Low" confidence predictions are barely above random chance.

Training Dynamics and Balanced Validation

Training financial models presents unique challenges, particularly the tendency to collapse toward predicting a single class. Our novel validation scoring function addresses this:

Where is the precision-recall balance metric:

And applies severe penalties for extreme prediction distributions:

if precision == 0 or recall == 0:

# Heavy penalty for predicting all one class

balance_penalty = 0.5

elif precision < 0.2 or recall < 0.2:

# Moderate penalty for extreme imbalance

balance_penalty = 0.3

This scoring function drives the model toward balanced predictions that maintain high accuracy:

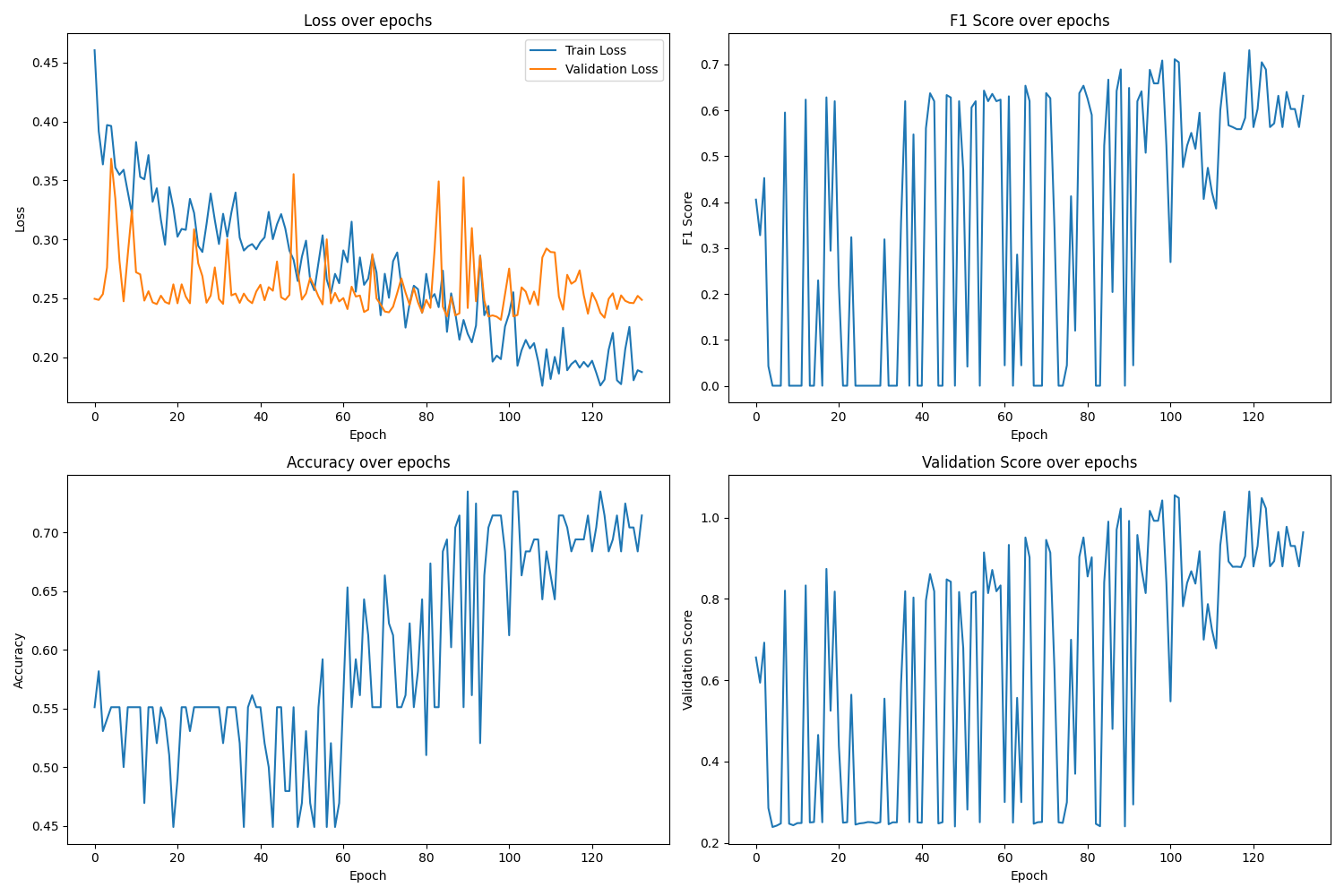

Training dynamics

Training dynamics

The plot above reveals how training progresses through multiple phases, with early fluctuations stabilizing into consistent improvements after epoch 80.

Model Architecture Details

Hanabi-1 employs a specialized architecture with several innovative components:

- Feature differentiation through multiple temporal aggregations:

- Last hidden state capture (most recent information)

- Average pooling across the sequence (baseline signal)

- Attention-weighted aggregation (focused signal)

- Direction pathway with BatchNorm for stable training:

- Three fully-connected layers with BatchNorm1d

- LeakyReLU activation (slope 0.1) to prevent dead neurons

- Xavier initialization with small random bias terms

- Specialized regression pathways:

- Separate networks for volatility, price change, and spread prediction

- Reduced complexity compared to the direction pathway

- Independent optimization focuses training capacity where needed

The model's multi-task design forces the transformer encoder to learn robust representations that generalize across prediction tasks.

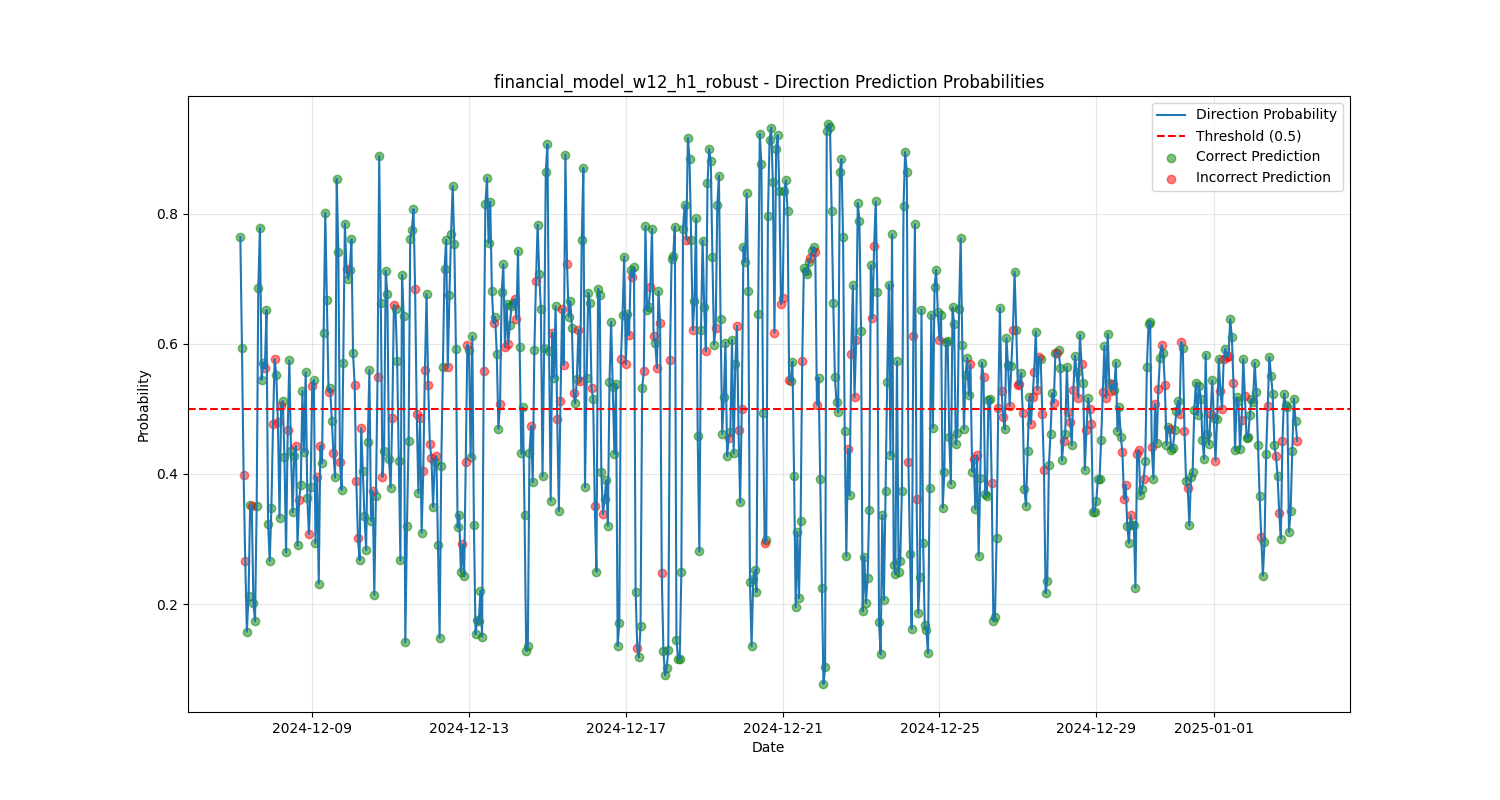

Prediction Temporal Distribution

Direction Probabilities

Direction Probabilities

The distribution of predictions over time shows Hanabi-1's ability to generate balanced directional signals across varying market conditions. Green dots represent correct predictions, and red dots are incorrect predictions.

Performance and Future Directions

Current performance metrics:

- Direction accuracy: 73.9%

- F1 score: 0.67

- Balanced predictions: 54.2% positive / 45.8% negative

Hanabi-1 currently operates on two primary configurations:

- 4-hour window model (w4_h1)

- 12-hour window model (w12_h1)

Both predict market movements for the next hour, with the 12-hour window model showing superior performance in more volatile conditions.

Future developments include:

- Extending prediction horizons to 4, 12 and 24 hours

- Implementing adaptive thresholds based on market volatility

- Adding meta-learning approaches for hyperparameter optimization

- Integrating on-chain signals for cross-domain pattern recognition

Conclusion

Hanabi-1 demonstrates that specialized, compact transformers can achieve remarkable results in financial prediction tasks. By focusing on addressing the unique challenges of financial data—class imbalance, temporal dynamics, and confidence calibration—we've created a model that delivers reliable signals even in challenging market conditions.

While the model can still be refined, we found that it’s a robust and important first step towards the definition and creation of even more capable financial models.

Follow the github repo for the current implementation and future upgrades: